Apple Just Broke a 40-Year Rule — What It Means for Your Semiconductor ETF

📋 Table of Contents

If you search “semiconductor ETF” right now, you’re going to find the same thing everywhere. SMH vs SOXX comparison tables. Expense ratios. Top 10 holdings. Maybe a note about how SOXQ is 15 basis points cheaper.

None of it tells you what actually happened last week. And that’s a problem — because what happened last week is the single clearest signal about semiconductor ETF positioning I’ve seen in 2026.

On June 25, Apple did something it hasn’t done in over 40 years. It raised prices on MacBooks and iPads mid-cycle — no new product launch, no spec bump, no keynote. The Mac Studio jumped from $3,999 to $5,299. A $1,300 increase. Overnight. MacBook Pro? Up $300. MacBook Air? Up $200. Even the little Apple TV streaming box went from $149 to $249 — a 67% jump.

Tim Cook called it “a hundred-year flood” and admitted, “I’ve never seen anything like it in any area in over 40 years.” Apple’s stock dropped 6% that day. Nearly $200 billion in market value — erased.

I’ve been tracking semiconductor supply chains as part of how I invest, and I’ll be honest: my first reaction to this was wrong. I thought it was an Apple-specific margin problem. It took me a day of digging before I realized what the price hike was actually signaling — and it changes the calculus for anyone holding a semiconductor ETF.

What Actually Happened at Apple

Apple has an unwritten rule, and it held for four decades. The price of a product is set at launch, and that’s it. If component costs rise mid-cycle, Apple absorbs them. That’s what the world’s best supply chain operation and a few hundred billion in cash buys you: pricing stability for the consumer.

That rule died on June 25, 2026.

Apple’s official statement was unusually direct: “The rapid expansion of AI data centers has created an extraordinary surge in demand for memory and storage… We have shielded our customers from these increases so far, but we have now reached a point where we need to begin raising prices.”

Translation: the DRAM and NAND flash memory that goes into every MacBook, iPad, and iPhone has gotten so expensive that even Apple — the company with the most feared procurement operation on earth — can’t eat the cost anymore.

But the statement left out the most important part. The part that changes the semiconductor ETF investment case.

The Real Reason: AI Ate Your MacBook’s Memory

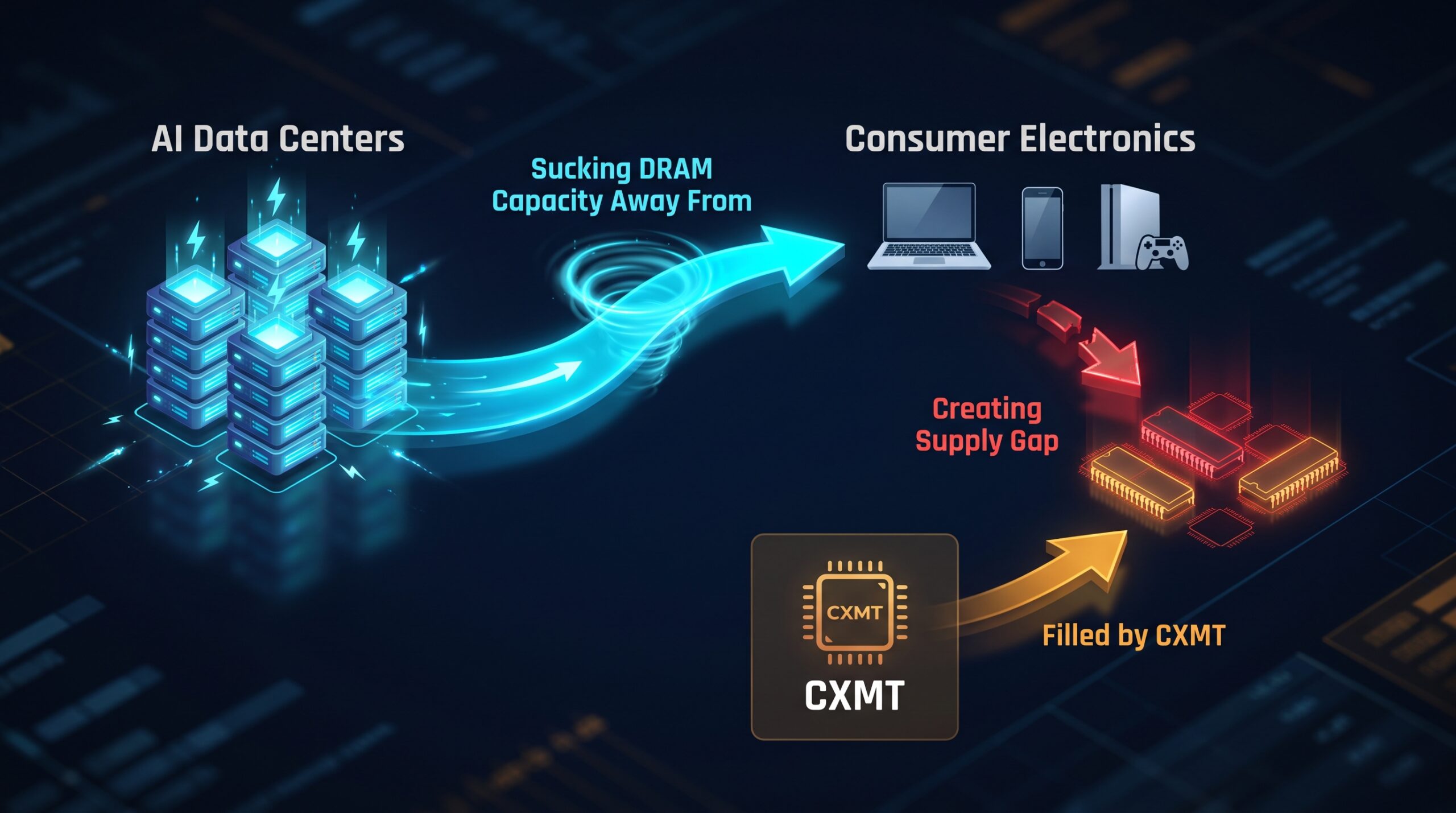

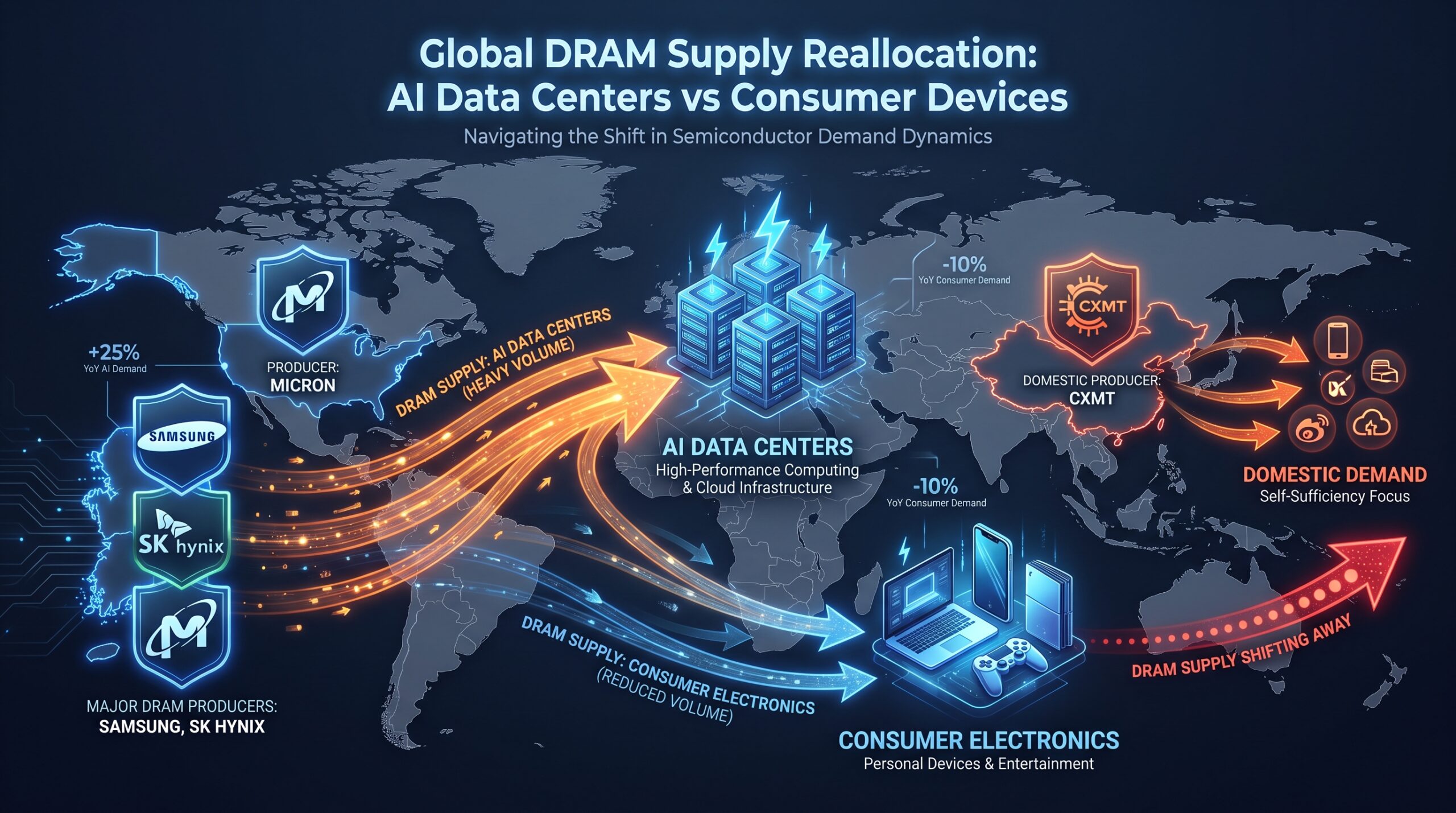

Three companies control roughly 95% of the world’s DRAM: Samsung, SK Hynix, and Micron. Over the past two years, all three made the same strategic decision. They shifted production capacity away from the standard DDR5 and LPDDR5 memory that goes into laptops and phones, and redirected it into High Bandwidth Memory (HBM) — the specialized, ultra-high-speed memory that NVIDIA’s AI GPUs require.

The economics driving this are extreme. HBM chips sell for 3 to 5 times more per wafer than standard DRAM, with profit margins north of 70%. Making HBM consumes roughly three times the silicon wafer capacity of standard DDR5 per gigabyte — what the industry calls the “die penalty.” And the buyers — Microsoft, Amazon, Meta, Alphabet — are signing multi-year contracts worth tens of billions, no questions asked.

Apple’s smartphone and laptop orders? Pushed to the back of the line.

Contract DRAM prices surged roughly 90% in Q1 2026 alone, then another 60% in Q2. The memory inside your next device is now about four times more expensive than it was three quarters ago. The memory chip shortage isn’t about factories failing to produce — it’s about allocation. The chips exist. The fabs are running hot. They’ve just decided your MacBook isn’t the priority anymore.

I used to think supply shortages meant “factories can’t keep up with demand.” This one is different. This is three oligopolists collectively choosing to serve a higher-margin customer. And there’s a class-action lawsuit alleging exactly that — that Samsung, SK Hynix, and Micron artificially restricted traditional DRAM supply to inflate prices under cover of the HBM transition. Whether the lawsuit succeeds or not, the dynamic it describes is real and visible in the pricing data.

Here’s why this matters for semiconductor ETFs specifically: every major DRAM producer sits inside SMH and SOXX. The memory shortage is inflating their revenues at a rate that has nothing to do with the business cycle. It’s a structural reallocation of the most fundamental computing component. And it won’t unwind in a quarter or two — S&P Global’s research suggests the supply-demand gap persists through at least 2028.

Why the Usual “China Dumping” Fear Is Wrong This Time

Every time I mention this thesis, someone brings up the same objection: “What about CXMT? Once Chinese memory makers scale up, they’ll flood the market and crash DRAM prices.”

I nearly made this exact mistake. I was ready to reduce semiconductor exposure because the China dumping narrative sounded so logical. Then I looked at what actually happened with tungsten.

China controls about 90% of the world’s tungsten — a metal essential for armor-piercing ammunition, cutting tools, drilling equipment, and semiconductor manufacturing. For years, the prevailing market assumption was: China will dump tungsten, prices will collapse. Every sell-side note repeated it.

What actually happened? China imposed export controls, nearly zeroed out commercial tungsten shipments, and then — this is the part that stopped me cold — started importing tungsten itself. From Rwanda. From Bolivia. From Portugal. Whoever would sell. Tungsten prices rose nine-fold in a year.

A 30-year tungsten trader told the market: “You will never see Chinese tungsten raw material return to global markets.”

The lesson reshaped how I think about every “China dumping” narrative: sitting on a mine doesn’t mean you have surplus to dump.

CXMT — ChangXin Memory Technologies, China’s largest DRAM maker — is on the Pentagon’s 1260H list of companies allegedly linked to the Chinese military. According to the Financial Times, Apple has been quietly lobbying the White House for over a month, asking for a guarantee that CXMT won’t be added to the Commerce Department’s Entity List. Because if CXMT gets added, American companies can’t buy from them — and right now, Apple desperately needs another memory supplier that isn’t one of the three oligopolists squeezing it.

CXMT’s Q1 2026 revenue hit roughly $7 billion — up over 700% year over year. The company just received approval for a Shanghai STAR Market IPO, aiming to raise approximately $4.3 billion. Three years ago it was burning cash. Today it’s the most important semiconductor company most American investors have never heard of.

But here’s what the “China dumping” crowd misses: CXMT’s entire output is being consumed by domestic customers — Alibaba Cloud, ByteDance, Tencent, Xiaomi, Oppo. China’s own AI infrastructure buildout and consumer electronics demand are eating every wafer CXMT can produce. The company’s market share is roughly 7.7% globally. It cannot meet domestic demand, let alone dump into global markets.

The irony is structural: Samsung, SK Hynix, and Micron abandoned standard DRAM to chase HBM profits, and in doing so, they handed their future Chinese competitor a lifeline. CXMT doesn’t need to catch up on HBM technology (it can’t — it lacks EUV lithography). It just needs to fill the vacuum the big three created in standard DRAM. And that’s exactly what it’s doing, at profit margins it never would have achieved in a normally supplied market.

The “ai bubble stocks” fear narrative that’s keeping some investors out of semiconductor ETFs is, in this specific case, built on an assumption about Chinese supply that doesn’t survive contact with data.

What This Means for Your Semiconductor ETF — Specifically

Let me translate the supply chain into actual positioning. Because if you’re holding a semiconductor ETF, you’re holding both sides of this equation.

The core holdings: SMH vs SOXX. In 2026, SOXX (or the cheaper SOXQ at 0.19% expense ratio) has outperformed SMH by roughly 20 percentage points. The reason, which most ETF comparison articles explain mechanically but not strategically: the rally has broadened beyond NVIDIA into mid-cap chip companies and equipment makers — exactly the kind of names SOXX weights more heavily. SMH puts ~15% in NVIDIA and ~10% in TSMC. A quarter of your position moves on two stocks. That concentration was a feature on the way up. It becomes a risk if AI sentiment wobbles. For a core holding right now, I lean SOXX or SOXQ — not because the expense ratio is lower, but because the memory supply story is a broadening catalyst, not a concentration catalyst.

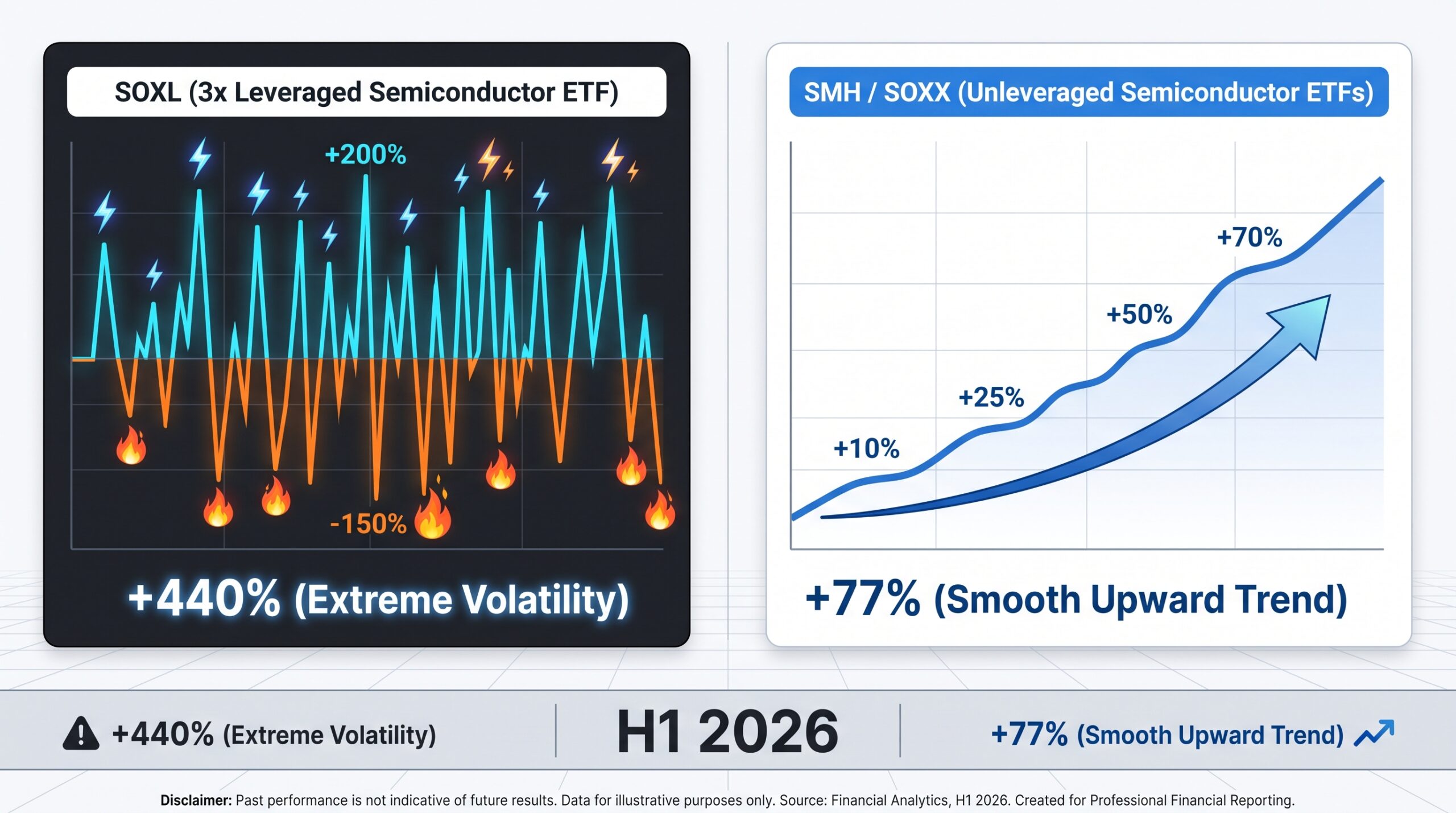

The memory pure play: DRAM ETF. If you specifically want exposure to the HBM and DRAM shortage thesis, there’s a vehicle for that now: the Roundhill Memory ETF (ticker: DRAM), which holds SK Hynix, Micron, and Samsung in concentrated form. It has roughly $16.7 billion in AUM and returned about 77% in H1 2026. This is a satellite position, not a replacement for a core semiconductor ETF — but it’s the most direct expression of the “memory is the new oil” thesis.

The China access play: KSTR. If you want indirect exposure to the CXMT story, the KraneShares SSE STAR Market 50 ETF (KSTR) is currently the only U.S.-listed fund that provides it. CXMT’s STAR Market IPO is one of the most anticipated listings in China — and KSTR will hold it once it lists. This is a higher-risk, higher-reward position — the same 1260H/Entity List uncertainty that makes the story interesting also makes it volatile. Size accordingly.

The one to handle with extreme caution: SOXL. SOXL returned +440% in H1 2026. That number is going to pull people in. Don’t let it. This is a 3x daily leveraged instrument — it is not designed for holding periods longer than days. I’ve made the mistake of treating leverage casually, and I’ll explain what that actually felt like in the next section.

Common Mistakes Semiconductor ETF Investors Are Making Right Now

Mistake #1: Treating SOXL like a long-term hold — and what an 80% drawdown actually feels like

There’s a famous r/wallstreetbets story about an investor who put $1 million into SOXL, watched it bleed to $200,000 during the 2025 tariff selloff, held through the devastation, and eventually cashed out at $7.5 million. The story got shared everywhere as inspirational.

What nobody talks about is what those months between $200K and $7.5M actually felt like. I’ve held through a leveraged drawdown — smaller than that, maybe 40% — and it was the worst few weeks of my investing life. I was checking the position at 2am. I was running the decay math in my head during meetings. I was constructing elaborate rationalizations for why I shouldn’t sell, when the rational reason to sell was staring at me. The physical feeling is somewhere between nausea and paralysis. You stop trusting your own judgment.

The guy who held from $1M to $200K to $7.5M got lucky — and he’s statistically a unicorn. Most people capitulate somewhere in the trough. Some never come back. Three times daily leverage, in a choppy market, silently bleeds value through volatility decay. SOXL dropped 23% in a single day on June 23. That’s not a buying opportunity — that’s a reminder of what the instrument is.

SOXL is a 1-3 day tactical tool. Your core semiconductor ETF position should be an unlevered vehicle. I use SOXQ. End of story.

Mistake #2: Thinking an ETF is automatically diversified

I learned this one the annoying way — by checking my portfolio after a rough NVIDIA earnings call and realizing my “diversified” SMH position had moved almost lockstep with NVDA. That’s not diversification. That’s concentration with extra steps. SMH puts over 15% in NVIDIA and another 10% in TSMC. A quarter of your “diversified” position moves on two companies. SOXX caps individual holdings at 8%, which is meaningfully better. If actual diversification matters to you, XSD — the equal-weight semiconductor ETF with 44 holdings — is worth a look. It’s smaller and less liquid, but no single stock can move the needle.

Mistake #3: Ignoring the VIX when trading leveraged semiconductor positions

This one actually cost me real money, and the mistake was embarrassingly simple. I was trading SOXL during a stretch when the semiconductor index was grinding higher but the VIX had crept above 25. The index finished the month up 3%. SOXL finished the month down. I didn’t understand why until I sat down and did the daily-reset compounding math.

SOXL thrives when the VIX is below 20 and the trend is consistently up — exactly the conditions of H1 2026, with the VIX hovering around 18.5. Once the VIX breaks 25, daily reset decay starts working against you even if the underlying index is flat to slightly up. If you’re going to touch a 3x instrument, the VIX is not optional context. It is the instrument’s operating manual. Check it before every trade. I do now — because I got tired of losing money to math I didn’t understand.

FAQ: Questions People Are Actually Searching

Is semiconductor ETF still a good investment in 2026?

It depends entirely on whether you understand what’s driving the returns. If you’re buying because the chart is trending up, you’re gambling — and BofA’s semiconductor bubble indicator sits at 0.91 out of 1.0. The Buffett Indicator (total U.S. market cap to GDP) is at 218%. These numbers are flashing caution.

But if you understand that the AI capex cycle has structurally reallocated memory supply — that this isn’t a demand spike but a capacity redirection that takes years to reverse — the fundamentals are stronger than most surface-level ETF analysis captures. The key is position sizing. A semiconductor ETF should be a satellite holding, not your entire portfolio.

SMH vs SOXX: which one?

In the current environment where the rally has broadened beyond NVIDIA, SOXX (or the cheaper SOXQ) has the edge. SMH’s heavy concentration in NVDA and TSMC was a tailwind in 2023–2024, and it will likely be a tailwind again if AI leadership re-concentrates. But right now the action is in mid-cap chip companies and equipment makers — and SOXX captures more of that. Over a 10-year horizon, they move together more than they diverge. The real decision is whether you want single-stock concentration risk in your sector ETF.

Is this an AI bubble?

Some signals are seriously flashing: $1.3 trillion evaporated from the semiconductor sector in a single week in late June 2026, and yet the Dow closed higher that week, small caps rose over 3%, and the VIX stayed at a calm 18.5. That’s rotation — not capitulation. The uncomfortable truth: nobody knows yet whether the $700 billion in committed data center capex from Microsoft, Amazon, Alphabet, Meta, and Oracle represents real end-user demand or mutual panic spending — “we have to build it because they’re building it.” That’s the question that separates a real cycle from a bubble. If you can answer it, you don’t need this article. If you can’t, that’s exactly why you stay sized appropriately.

Final Thoughts

I didn’t expect an Apple price hike to become the most important semiconductor investing signal of 2026. But that’s how supply chains work as information systems — the biggest tells don’t come from earnings calls or sell-side notes. They come from the companies at the end of the chain, the ones that can no longer hide the cost.

Apple breaking its 40-year pricing discipline isn’t a consumer tech story. It’s a live stress test of the global memory supply — and the test result says the pressure isn’t easing.

The signal I’m watching next: whether the White House grants Apple the assurance it’s seeking on CXMT, or whether political opposition (Congressman Moolenaar has already called the idea “a grave mistake”) kills the deal. If Apple gets its guarantee, it’s a powerful validation that even U.S. national security hawks recognize the memory supply chain is too tight to ignore. If it doesn’t, Apple’s pricing pressure intensifies — and the three oligopolists get even more pricing power. Either outcome has consequences for semiconductor ETF holders.

Your semiconductor ETF is holding companies on both sides of this equation: the memory producers profiting from scarcity, and the device makers getting squeezed by it. Understanding which side is winning — and why — is the difference between informed positioning and hoping the chart keeps going up.

That’s the kind of supply chain signal I track. If you find this lens useful, you might want to bookmark this page — I don’t cover the surface-level ETF comparison stuff you can get anywhere else.

By the way — a friend of mine runs a Telegram channel where he shares trade ideas and market observations, including moves around semiconductor cycles and macro supply chain events like the one in this article. It’s low-key, no hype. If that sounds like something you’d check out: t.me/+kSMilTpNdcZlNjYx