SpaceX IPO: 3 Events That Reveal Who This Market Is Built For

In the span of four days, the U.S. stock market delivered three events that looked completely unrelated — until you put them on the same table.

June 1. Andrew Left, the founder of Citron Research, gets convicted by a federal jury on 13 counts of securities fraud. For years, he shouted stock picks on Twitter while running the opposite trade behind the scenes — taking positions before his posts moved prices, closing them the same day, and boasting his tactics were like “taking candy from a baby.” A retired firefighter testified he lost $110,000 from his retirement funds acting on Left’s public calls. Left now faces up to 25 years.

June 4. The Pattern Day Trader rule — a 25-year-old regulation built after the dot-com crash to stop small accounts from blowing themselves up — gets formally repealed. For the first time since 2001, accounts under $25,000 can day trade without restriction. No more three-trades-per-week cap. No more 90-day freezes.

June 10–12. SpaceX prices the largest IPO in history. $135 per share. Ticker SPCX. Roughly $75 billion raised at a $1.77 trillion valuation — more than double Saudi Aramco’s 2019 record. And Fidelity, a broker that normally requires $10,000 to $500,000 to access IPOs, slashes the threshold to $2,000. Schwab keeps its $100,000 minimum. Robinhood and SoFi let you in for pocket change.

One guy who used retail as exit liquidity goes to prison. Two doors — one regulatory, one financial — swing wide open for retail investors in the exact same week.

I spent several days pulling apart the S-1 filing, comparing broker policies, and cross-referencing the timelines. My honest take? The three events are probably a coincidence. The PDT repeal was approved in April after months of regulatory process. Andrew Left was indicted in 2024 and the jury took two days to deliberate — nobody timed that. SpaceX picked its own business calendar.

But here’s the thing: whether it’s a coincidence or a conspiracy doesn’t actually matter. What matters is what the convergence reveals about the structure you’re about to participate in — and whether that structure treats you like a guest or the pre-paid dinner.

Table of Contents

Three Events, One Week

Let me walk through each one, because the order matters.

Event one: the enforcement backdrop. I remember watching Citron Research videos years ago, early in my trading journey. Left had this confidence — pointing at companies on CNBC, declaring their valuations were fake, their books cooked, their business models a house of cards. He was right about some of them. He famously called out Chinese real estate giant Evergrande in 2012, years before it collapsed. He took down Valeant Pharmaceuticals in 2015, exposing a channel-stuffing scheme that later got called “the pharma Enron.” The guy was a genuine fraud-hunter.

But according to prosecutors, he was also running a side business: take a position, publish a report, close the position the same day on the price move he himself created. Give select hedge funds advance access to the research in exchange for profit-sharing — disguised through fabricated invoices. He told people his tactics were like “taking candy from a baby.” The jury convicted him on 13 of 17 counts.

The message lands on June 1, loud and clear: the era of “say one thing, do another” now has a prison sentence attached.

Event two: the doors open. The PDT rule was created in 2001 for a reason. The dot-com bubble had just vaporized a generation of small retail accounts. The SEC looked at the carnage and said: if you don’t have $25,000 in your account, you probably shouldn’t be day trading every day. It was a wall. Annoying, yes. But it was also a guardrail.

I got flagged under it once. Early in my trading, I was in and out of a position three times in a single week — nothing reckless, just active. The fourth trade never went through. My account got frozen for 90 days. No warning, no phone call, just a lock screen. I was furious. It felt like the system was treating me like a child.

On June 4, that wall came down. And I’ll be honest — part of me felt relieved. Finally, small accounts get the same flexibility as the big players.

But the timing is worth sitting with. The same week the guardrail disappears, the most volatile IPO in history goes live. If you’re not setting your own rules now, nobody else will.

Event three: the welcome mat. Fidelity’s standard IPO minimums range from $10,000 to $500,000. For SpaceX, that became $2,000. A 99.6% reduction. As one commenter online put it: “From $500K to $2K — this isn’t generosity. This is them realizing they need retail for exit liquidity.”

That comment stung because it echoed something I was already feeling. When someone who’s been charging you cover at the door suddenly waves you in for free, the right question isn’t “how generous.” It’s “what changed?”

The Lock-Up Nobody Is Talking About

This is where most coverage stops and where the real story lives.

I read the S-1. Here’s what it actually says.

SpaceX is reserving approximately 30% of IPO shares for individual investors. There’s an old Wall Street saying: the more shares they leave for retail, the less institutions wanted them. I don’t know if that’s true here. But 30% is genuinely unusual for a deal this size.

The part that stopped me cold was the lock-up schedule.

Elon Musk is locked for 366 days. He cannot sell a single share — not if the stock doubles, not if it crashes, not at all — for a full year plus one day. That’s real. I respect it. If the guy everyone worries will dump and crash the stock has voluntarily chained himself to the mast, that says something.

But — and this is the but that gets skipped in every headline — up to 5% of the IPO goes through something called the Directed Share Program. The S-1 describes it as shares set aside for “certain employees and persons” designated by company executives. These shares carry zero lock-up. No days. Not one. They can be sold the moment the stock opens, while you — the retail buyer who got in through Fidelity — cannot sell for at least 15 days without triggering a penalty. On Robinhood or SoFi, it’s 30 days.

Five percent of a $75 billion raise. That’s up to $37.5 billion in potential Day 1 selling pressure — from people whose names you will never know — while your shares sit frozen in your account.

Then the staggered unlocks begin. Roughly 45 to 60 days post-IPO, after Q2 earnings, up to 20% of locked shares release. If the stock rises 30% above the IPO price for five trading days, another 30% unlocks. Days 70, 90, 105, 120, and 135 each add 7% more. Q3 earnings around October or November adds 28%. Day 180 unlocks everything except Musk’s shares.

Semafor recently reported that SpaceX’s own bankers are actively worried about this — $1 trillion worth of stock needs to be eased into the market over months, not dumped all at once, or the stock gets crushed. They’re considering phased unlocking tied to price and volume thresholds, similar to what Alibaba tried in 2014. Alibaba still sold off before its final cliff anyway.

Here’s what I keep coming back to: the person you should worry about can’t sell for a year. The people you’ve never heard of can sell on Day 1. The mismatch is either brilliant legal engineering or the market’s way of telling you exactly whose interests this structure was designed to serve.

The Nasdaq Fast-Track: The Invisible Hand You Didn’t See

There’s one more piece to this that most people miss, and it’s arguably the most important.

Nasdaq normally requires companies to trade for several months before qualifying for major index inclusion — the Nasdaq-100, the funds, the ETFs. For SpaceX, Nasdaq cut that window to just 15 trading days.

This isn’t a rumor. It’s a documented rule change.

What it means: roughly two weeks after SPCX starts trading, every Nasdaq-100 index fund, every ETF that tracks it, every 401(k) with passive allocation to large-cap stocks — they’re all forced to buy. Regardless of price. Regardless of valuation. The computers don’t care if Morningstar says the company is worth half what it’s trading at.

This creates a massive, guaranteed wave of buying pressure during the exact window when retail holders are locked and cannot sell. The price goes up — not because the market has “discovered” SpaceX’s true value, but because mechanical buying meets a 4% float with retail locked on the sidelines.

When insiders and Directed Share Program recipients can sell on Day 1, and index funds are forced to buy 15 trading days later, and you can’t touch your shares for 15–30 days — who exactly is the bridge between those two groups? What role does your position play in that sequence?

I’m not saying it’s a conspiracy. I’m saying the mechanics are the mechanics, and they don’t require a conspiracy to produce a specific outcome.

Coincidence or Conspiracy?

I went into this wanting the conspiracy to be true. It’s a better story. “Musk controls the regulators, they cleared out the short sellers, then opened the floodgates for retail to come hold the bag.” That narrative writes itself. It’s emotionally satisfying. It confirms everything you already suspect about how the game is rigged.

I couldn’t make the facts fit.

The PDT repeal was filed in January, approved in April, and scheduled for June 4 months before anyone knew SpaceX would price that week. It was never about SpaceX. It was a coincidence.

Andrew Left’s trial was on the court’s calendar, not Elon Musk’s. The jury deliberated for two days. The verdict landed June 1. Nobody engineered that.

SpaceX picked its own IPO date based on its own commercial needs. The company has been private for over 20 years. It needs billions for Starship and Starlink. That’s not a conspiracy — that’s a business.

And yet.

A guy who used retail as exit liquidity goes to prison. Two doors swing open for retail in the same week. The largest IPO in history arrives with a lock-up structure that prevents you from selling while letting a hand-picked list of insiders out — and Nasdaq changed its own rules to make sure index funds line up as buyers while you’re still sitting on your hands.

Calling all of it “coincidence” feels almost irresponsible. My honest opinion: nobody is in a room pulling levers. But the effect is indistinguishable from if they were. Three independent forces, each on its own timeline, converged to create a market structure where retail investors are being enthusiastically invited into the biggest IPO ever — with the freedom to trade actively and the obligation to hold while others sell.

Your time horizon is the only variable that determines which side of that structure you land on.

Mistakes I’ve Made (and Seen Others Make) Around Big IPOs

I wasn’t always the guy reading S-1 filings. I learned some of this the hard way.

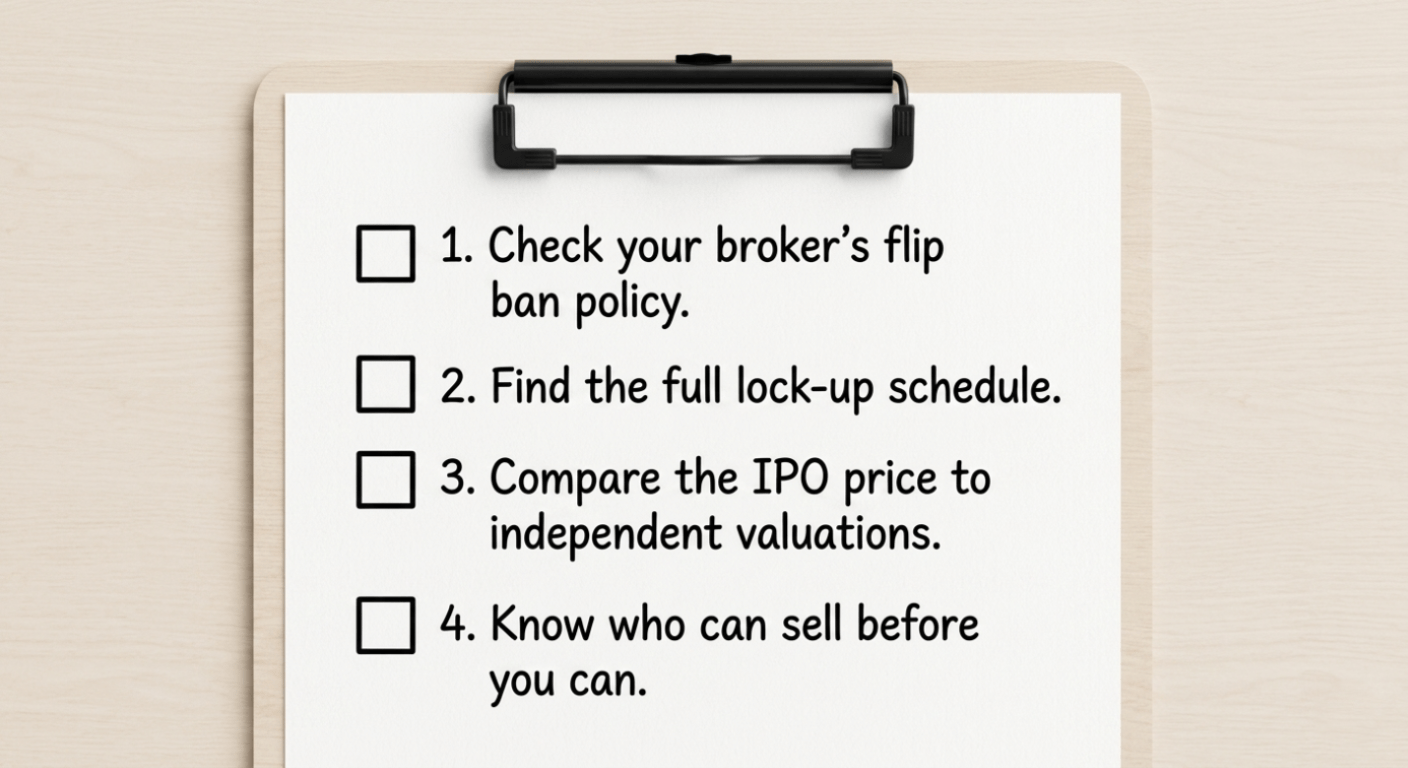

Mistake 1: Not checking your broker’s flip ban before clicking buy. Fidelity’s rules are public: sell within 15 days, you get banned from IPOs for 6 months. Do it again, it’s a year. Do it a third time, it’s permanent — you’re done with every Fidelity IPO forever. Robinhood and SoFi enforce 30 days. So let’s say the stock opens at $135 and spikes to $190 on Day 2. You hit sell, feel like a genius, and two weeks later a letter arrives. You are now barred from participating in every future IPO on that platform. That’s not a hypothetical — it’s in the terms you clicked through without reading.

Mistake 2: Confusing “affordable” with “fairly priced.” $135 per share and a $2,000 minimum feels like you’re getting access, not getting played. But run the numbers. Morningstar’s independent valuation puts SpaceX at roughly $780 billion — less than half the IPO price. The company lost over $4 billion in Q1 2026. At this price, you’re not buying a rocket company. You’re buying an AI narrative attached to a rocket company, priced as if the AI revenue already exists. Goldman’s bull case assumes xAI revenue grows 100× by 2030. That might happen. But understand: at $135 a share, it needs to happen for the price to make sense.

Mistake 3: Believing the headline version of “everyone is locked.” The headline says “Musk locked for one year.” The headline skips the Directed Share Program entirely. The S-1 is a public document. The lock-up schedule is written in plain English. But almost nobody reads it — and so almost nobody knows that a hand-picked group can sell on Day 1 while you’re locked for 15 to 30 days. Read the document. Your edge as a retail investor isn’t speed or access. It’s the willingness to do the reading everyone else skips.

Mistake 4: Thinking the guardrail removal is pure freedom. I told you about my PDT freeze — that 90-day lockout that felt like punishment. What I didn’t tell you is that during those 90 days, I watched a position I would have panic-sold at a loss recover and run 40% higher. The freeze forced me to hold. I got lucky. But the point is: the rule existed because regulators had decades of data showing small accounts blow up faster when there’s no friction. If you’re entering the most volatile IPO in history with no external guardrails, you’d better have internal ones. Write down your max position size. Write down your stop-loss. Write down your max trades per week. The market won’t protect you anymore.

Mistake 5: Forgetting the precedents. Beyond Meat went public in 2019 at $25. Within three months, it hit $235. The underwriters waived the lock-up early so insiders could sell into the mania. Today, Beyond Meat trades at roughly 60 cents. Not $60 — sixty cents. The people who bought at $235 because “plant-based meat is the future” weren’t wrong about the trend. They were wrong about the structure they were participating in. The narrative was real. The mechanics ate them anyway.

A Note for Crypto Traders Crossing Over

If you came to this article from the crypto world — you’re used to permissionless markets, 24/7 trading, no broker gatekeepers, no PDT rules, no lock-up periods — let me tell you something directly.

This is not that.

In crypto, when you buy a token at launch, you can sell it 30 seconds later if you want. The market is always open. The rules are the same for everyone. The playing field is flat — sometimes brutally so, but flat.

In the traditional IPO world, the playing field is tiered. Some people get shares before you. Some people pay less than you. Some people can sell before you. Some people are forced to buy after you. The order of operations — who buys when, who sells when, who’s locked when — is the entire game. And it’s all disclosed in documents that most people never open.

The skills that make you successful in crypto — pattern recognition, risk management, not getting emotionally attached to narratives — those transfer. But the structural awareness has to be rebuilt from scratch. In this world, the rules are written in the fine print, and the fine print is not on your side by default.

FAQ

Is the SpaceX IPO a trap for retail investors?

Not in the fraud sense. Everything I’ve described — the Directed Share Program, the lock-up schedule, the flip bans, the Nasdaq fast-track — is disclosed in the S-1. It’s not hidden. It’s public. The question isn’t whether someone’s lying to you. The question is whether the structure, even when fully disclosed, creates a role for retail that you’re comfortable playing. If you’re a long-term investor who can hold through the staggered insider unlock waves over 6 to 12 months, the 15-day flip ban is irrelevant to you. If you’re trying to flip in the first week, you’re structurally disadvantaged and the structure was not designed for you.

Why did Fidelity lower its IPO minimum so dramatically?

Fidelity hasn’t explained beyond citing “increased share availability.” Here’s the math: SpaceX needs to raise roughly $75 billion. At a $1.77 trillion valuation for a company that lost billions last quarter, institutional demand may not fill the entire book. Retail demand — distributed across millions of small accounts, many of whom trust the Musk brand — fills the gap. Whether that’s democratization or a liquidity need dressed up as democratization depends on how cynical you are.

Should I buy SpaceX stock on IPO day?

I’m not going to tell you what to do. I don’t know your account size, your risk tolerance, or your time horizon. What I will tell you is this: the people who get hurt in IPOs are almost always the ones who didn’t plan their exit before they entered. Know your broker’s flip ban. Know the lock-up schedule. Know the valuation gap. Know who can sell before you can and when. If you understand all of that and still want in — that’s your call, made with eyes open. That’s all I’m trying to give you.

Final Thoughts

SpaceX, as a company, is genuinely remarkable. Reusable rockets landing on drone ships in the middle of the ocean. Starlink connecting the unconnected. Engineers pushing aerospace forward at a pace that makes legacy contractors look like they’re standing still. I have enormous respect for what they’ve built.

But SPCX the stock is a financial instrument. At this valuation, with a 4% float, with a lock-up schedule that lets a hand-picked 5% sell on Day 1 while you can’t, with Nasdaq fast-tracking index funds to arrive as forced buyers during your lock window — this stock is a mechanical construct. And mechanical constructs don’t care about Mars.

The question isn’t “is SpaceX a good company.” It never was.

The question is: when enforcement, deregulation, and the largest IPO in history all seem to be pointing retail investors toward the same door in the same week — who is that door actually meant for?

Your time horizon decides your answer. If you’re a short-term speculator planning to flip in the first week, the structure was not built for you. If you’re a long-term investor willing to ride through 12 months of staggered unlocks and valuation settling, this might genuinely be a historic opportunity. Either way, you now understand the mechanics better than 99% of the people talking about this online.

I’m Alan. I read the filings, cross-referenced the lock-up schedules, and checked the historical precedents — so you don’t have to. If this kind of honest, document-first market breakdown is what you’ve been looking for, bookmark this site. I do this for every major market event.

No hype. No fear. Just the mechanics.