AI Bubble Burst: The $80B Signal Hidden in Alphabet’s Raise

If you’ve been watching the AI market this year, you’ve probably felt it. That knot in your stomach when Nvidia takes the stage in Taipei, lights blazing, Jensen Huang telling the world he’s “reinventing the PC.” And then — on the exact same day — in a much darker room in Silicon Valley, Alphabet quietly files the largest equity capital raise in U.S. corporate history.

Let that sink in. Google’s parent company earned $62.6 billion in net profit last quarter and pulled in $45.8 billion in operating cash flow from a business that generates roughly $5 billion in cash every single day from operations. And it’s still stretching out its hand for $80 billion.

A year ago I would have read that headline, felt a brief spike of fear, and made a reactive trade I’d regret by the next morning. Today, after months of reading every footnote in these filings, I read it differently. Here’s what I’ve learned — and what I believe every retail investor needs to understand before the next domino falls.

Table of Contents

What’s Actually Happening: The $80 Billion Raise

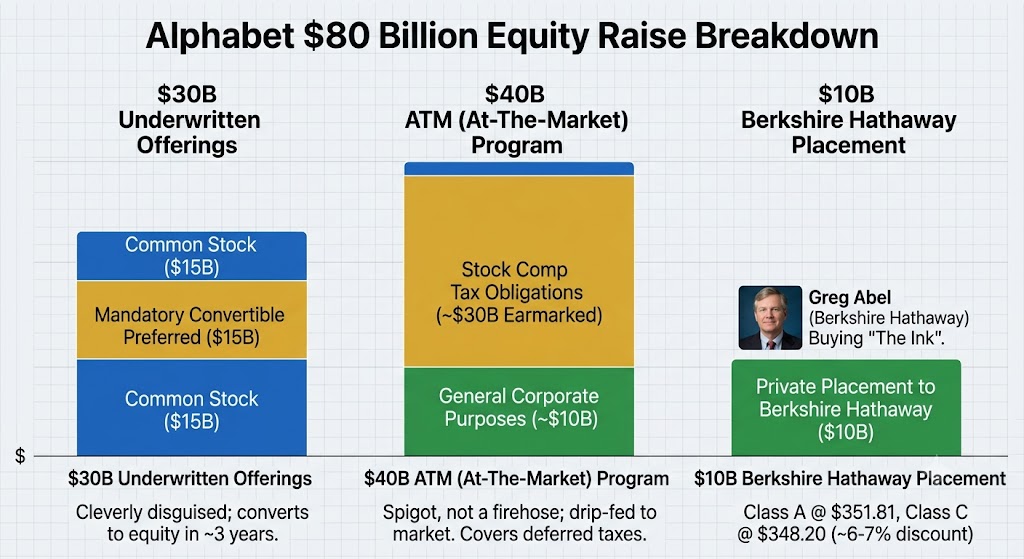

The $80 billion isn’t a single check. It’s three separate mechanisms, and each one tells a different story.

The first tranche — roughly $30 billion — is a standard underwritten offering, split between common stock and mandatory convertible preferred shares. The convertibles are cleverly disguised: they pay a coupon now like ordinary debt, then automatically convert into equity after about three years. The near-term earnings optics look cleaner. The dilution arrives later, quietly.

The second tranche is a $40 billion “at-the-market” program set to launch in Q3. Alphabet will drip-feed new shares into the market — a spigot, not a firehose — selling more when the stock is strong, less when it dips. But here’s the detail that made me stop and re-read the filing twice: roughly $30 billion of that ATM money is not earmarked for new AI chips or data centers. It’s designated to cover the income tax obligations on employee stock-based compensation. When Google employees’ RSUs vest and the company withholds taxes at the 22% supplemental rate — often well below the 32-37% the employee actually owes — Alphabet fronts the cash to the IRS and then replenishes its balance sheet by selling new shares into the market. In plain English: a large slice of this historic “AI funding” raise is paying the tax man for stock grants that were handed out years ago.

The third tranche is a $10 billion private placement to Berkshire Hathaway. Greg Abel — now steering Berkshire after Buffett’s retirement — bought Class A shares at $351.81 and Class C at $348.20, roughly a 6-7% discount to the prior close. While most of us were scrolling panic tweets, Abel was writing one of the largest checks of his career. We’ll come back to why.

The $36.9 Billion Paper Profit Nobody’s Talking About

Before we get to what this raise means, there’s another layer you need to see — because it changes how you read Alphabet’s “record profit” entirely.

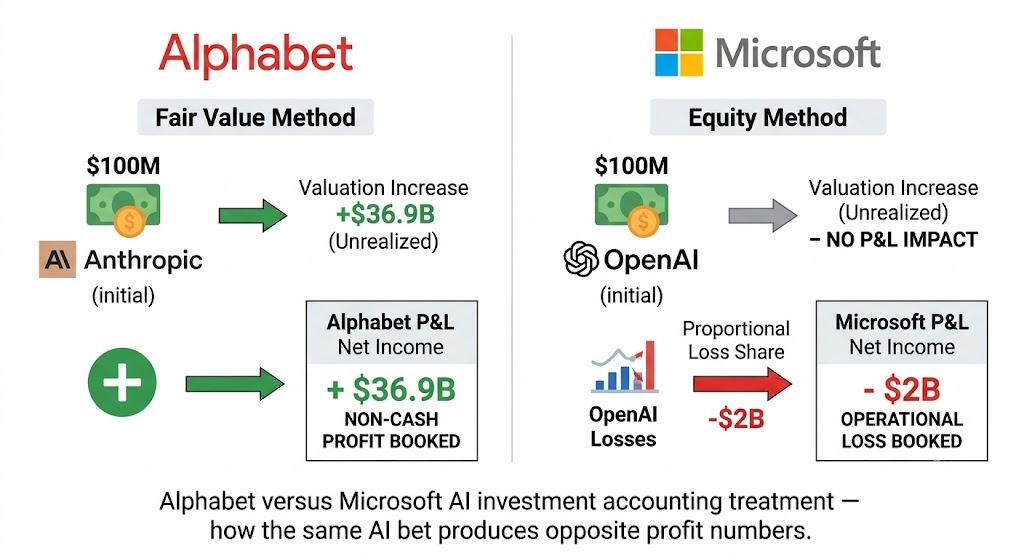

That $62.6 billion Q1 net profit headline? It includes a $36.9 billion unrealized gain on equity investments, almost entirely from Alphabet marking up the value of its stake in Anthropic after a new funding round set a higher valuation. That’s not cash. Alphabet didn’t sell a single share. But under mark-to-market accounting rules, when the company you invested in raises money at a higher price, you book the paper gain as profit — even though zero dollars changed hands.

Here’s where it gets genuinely strange. Alphabet uses the fair value method for Anthropic: valuation goes up → profit flows directly to net income. Microsoft, meanwhile, uses the equity method for OpenAI: it books a proportional share of OpenAI’s losses, while OpenAI’s soaring valuation to roughly $500 billion produces no profit benefit whatsoever in Microsoft’s P&L.

Two companies. Same AI investment thesis. Radically opposite accounting outcomes — and neither one has anything to do with actual cash generated by the underlying AI businesses.

Goldman Sachs recently flagged that both Alphabet and Amazon materially inflated aggregate S&P 500 earnings growth with gains like these. The implication isn’t fraud. It’s that a meaningful slice of the “AI profit miracle” you’re reading about in headlines is an accounting artifact. And accounting artifacts — unlike real cash flow — can reverse just as fast as they appeared.

I wish I had understood this six months ago. It would have saved me from making the very mistake I’m about to describe.

Why This Matters Right Now

Here’s why I can’t stop thinking about Alphabet’s raise — and why I believe it’s one of the clearest AI bubble burst signals available to retail investors.

Alphabet spent years doing something that broadcasted confidence: it used excess cash to buy back its own stock, shrinking the share count and silently enriching every remaining shareholder. That was the signal. We’re so profitable we don’t know what to do with the money.

That signal has now flipped. Alphabet is simultaneously issuing $80 billion in new equity, tapping debt markets for nearly $48 billion in bonds across multiple currencies and maturities — including a 100-year bond — and boosting its dividend by 5%. One hand is paying shareholders. The other hand is asking the market for more money. It’s internally contradictory, and the market felt it: the stock dropped about 2% after-hours on the announcement.

But the contradiction itself is the real signal. When the least cash-constrained company in the group — with $126 billion in cash and marketable securities on its balance sheet — becomes the first to aggressively tap both equity and debt markets for AI spending, the question is not whether Alphabet can afford it. The question is: who’s next? Microsoft? Amazon? Meta? If other money printers follow, it’s no longer a buying opportunity. It’s a warning flare.

Ken Griffin, who runs Citadel, has warned that the AI revolution may take 20 to 30 years to fully play out — not the 3 to 5 years current market valuations imply. Jamie Dimon has used the word “exuberance” — a term Alan Greenspan famously deployed in 1996, four years before the dot-com bubble actually burst. These aren’t perma-bears. These are people who survived every market cycle by knowing the difference between a story and a spreadsheet.

How to Read the Signals Like an Insider

After watching this unfold and making my own share of expensive errors, I’ve settled on two indicators I now track obsessively. Neither requires a Bloomberg terminal, and together they’ve become my personal early-warning system.

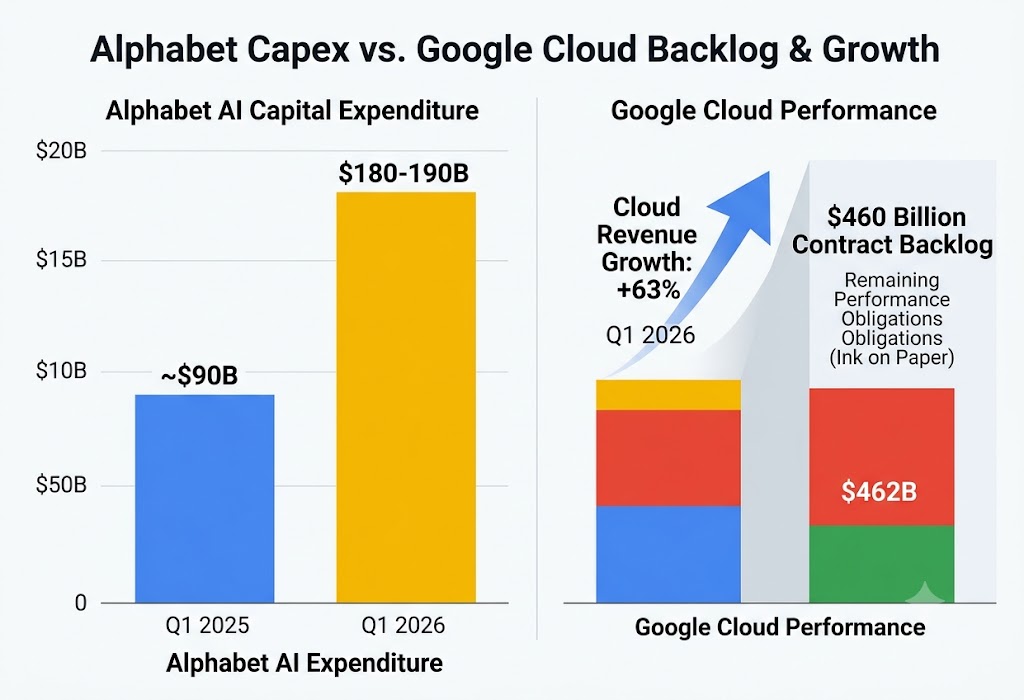

Indicator 1: Google Cloud’s backlog. Alphabet’s remaining performance obligations — signed, non-cancelable contracts — hit $462 billion in Q1, nearly doubling in a single quarter. Over half is expected to convert to revenue within 24 months. This isn’t a forecast. It’s ink on paper from enterprise customers who have already committed. If that number keeps growing in the next two quarterly reports, it means real, external demand exists — independent of the AI funding bubble. If it stalls or contracts, the AI capex machine is building capacity nobody actually ordered.

Indicator 2: Who else starts issuing stock and debt. This one is my secret weapon. I now maintain a simple rule: if another historically cash-rich tech giant announces a major equity raise for AI infrastructure, I don’t wait for sell-side analysts to weigh in. I tighten my stops immediately. Alphabet went first because it’s the strongest — $101.2 billion in trailing 12-month free cash flow and $126 billion in cash. If the strongest needs help, the weaker ones may not be far behind.

I also now apply one filter to everything I read about AI stocks: is this buyer purchasing “the story” or “the ink”? Most of us — and I include my own past trades here — are buying a narrative. Nvidia’s stage lights. The promise of AGI. The fear of being the only person not getting rich. But Berkshire Hathaway under Abel is buying something entirely different: $462 billion in black-and-white contractual commitments from enterprise customers who have already signed purchase orders. That’s not a bet on AI hype. That’s a bet on ink.

Mistakes That Cost Investors Real Money

I’ve made every mistake in this section. Not hypothetically. With my own money, my own stomach, my own late-night brokerage-app-open-in-the-dark sessions where you check the number for the third time hoping it’s magically changed.

Mistake 1: Reacting to a financing headline before reading the structure. When I first saw “Alphabet raises $80 billion,” my instinct was uncomplicated — dilution is bad, sell. I nearly hit the button. What I failed to check was that Berkshire was simultaneously buying $10 billion at a discount through a private placement. The headline was half the story. The structure — who was buying, at what price, through what mechanism — was the part that actually mattered. Now I read the filing, not the tweet. It takes twenty extra minutes and I’ve never regretted it.

Mistake 2: Chasing a hot AI-related stock without checking the dilution counter. I once bought shares of what I believed was a smart AI infrastructure play. The breakout looked clean. The chart was perfect. Forty-eight hours later, the company filed a surprise $500 million offering, and the stock cratered 30% in a single session. I didn’t know what a diluted share count was, let alone how to find it on page 47 of a 10-K. As Andrew Sather has explained, companies are finding increasingly creative ways to dilute shareholders — and “the risk shows up on page 47 of a 10-K, not in a headline.” Now I check three numbers before any position: diluted share count growth versus revenue growth, stock-based compensation as a percentage of revenue, and any convertible debt triggers hidden in the footnotes. If your share of the cake is shrinking faster than the cake is growing, you’re not investing. You’re funding someone else’s exit.

Mistake 3: Letting FOMO override my time horizon. Figma IPO’d at $33 in July 2025, opened at $115, and eight months later sat at $22 — down 81% from its peak and 33% below its IPO price. What most retail investors didn’t know — and what I didn’t know at the time either — was that the lockup agreement contained a hidden trigger: if the stock traded 25% above the IPO price for 5 consecutive trading days, 25% of locked shares would release after just 36 days instead of the standard 180. The stock crossed that threshold on day one. The CEO authorized the sale of 3 million shares four days after the IPO. Insiders were selling at ~$80 while retail was still buying the breakout. As one trader at EliteTrader put it, “the market’s underlying logic had changed, but I was still using an old map.”

FAQ: Your Biggest AI Bubble Questions

Is the AI bubble going to burst in 2026?

I don’t think it’s a binary yes or no. What I track instead: is Alphabet’s Cloud backlog still growing quarter-over-quarter, and has any other historically cash-rich tech giant followed Alphabet into equity markets? Those two answers will tell you more — and sooner — than any analyst report.

Why is Alphabet raising money when it’s so profitable?

Its AI capex guidance nearly doubled in a year — from roughly $90 billion to $180-190 billion — and the company has explicitly said the number will keep climbing. Even the most profitable company on earth can’t self-fund that rate indefinitely. But critically, a large slice of the $80 billion figure isn’t going to new AI infrastructure. Roughly $30 billion of the ATM program is allocated to covering tax obligations from employee stock grants. And Alphabet’s headline “record profit” includes $36.9 billion in non-cash, unrealized gains from marking up its Anthropic stake — paper profits that could reverse just as mechanically as they appeared.

Is Nvidia a bubble?

Michael Burry has called Nvidia’s AI financing structure “Fugazi,” pointing to complex off-balance-sheet vehicles where Nvidia invests in the same SPVs that buy its GPUs, creating what he sees as a self-referential revenue loop. At the same time, Nvidia’s PEG ratio sits below 1.0 — a level value investors typically consider undervalued. Both data points can be true simultaneously. The question isn’t whether Nvidia is objectively a bubble. The question is whether the end customers paying for its GPUs are generating revenue from sources outside the AI funding circle itself — or whether the whole thing is, as one NBER study found for 90% of firms, producing no measurable productivity gain.

Final Thoughts

There’s a metaphor that has stuck with me since the day Alphabet announced this raise. On one side of the world, Taipei — bright stage lights, Jensen Huang unveiling the next generation of AI hardware, cameras flashing, stock tickers flicking upward. On the other side, a quiet back room in Silicon Valley where an $80 billion invoice is being prepared and $36.9 billion in paper profits are getting booked without a single dollar changing hands.

The stage lights are designed to make you feel something. The invoice is what you should be reading.

The AI infrastructure buildout might be the most consequential investment cycle of our lifetime. Or it might be a self-referential loop: chip makers funding AI startups that buy chips from chip makers, cloud providers issuing compute credits that get recognized as revenue, and two companies invested in the same AI startup booking entirely different profit numbers based purely on their choice of accounting method.

Ken Griffin says the real transformation could take 20 or 30 years. He might be right. He might be early. But what I’ve learned — the hard way, with my own money, at hours of the night I’d rather not count — is that you don’t need to predict the future to protect yourself from it. You just need to know which numbers actually carry signal, which headlines are designed to trigger a reaction rather than a thought, and whose money is actually at risk when the invoice finally comes due.

Start tracking Alphabet’s Cloud backlog next quarter. Watch which money printer stretches out its hand next. And always — always — read the footnotes before you read the news.

Ready to Take the First Step?

Join our community for daily market news. Curious about our strategy? Preview 8-15 daily short-term trade setups in the Signals channel — new users who join via the "Trade Signals" button automatically receive a $59/month pass. Prefer a personal conversation? Contact us anytime.