SpaceX IPO: A Measuring Stick Every Retail Investor Needs Before June 12

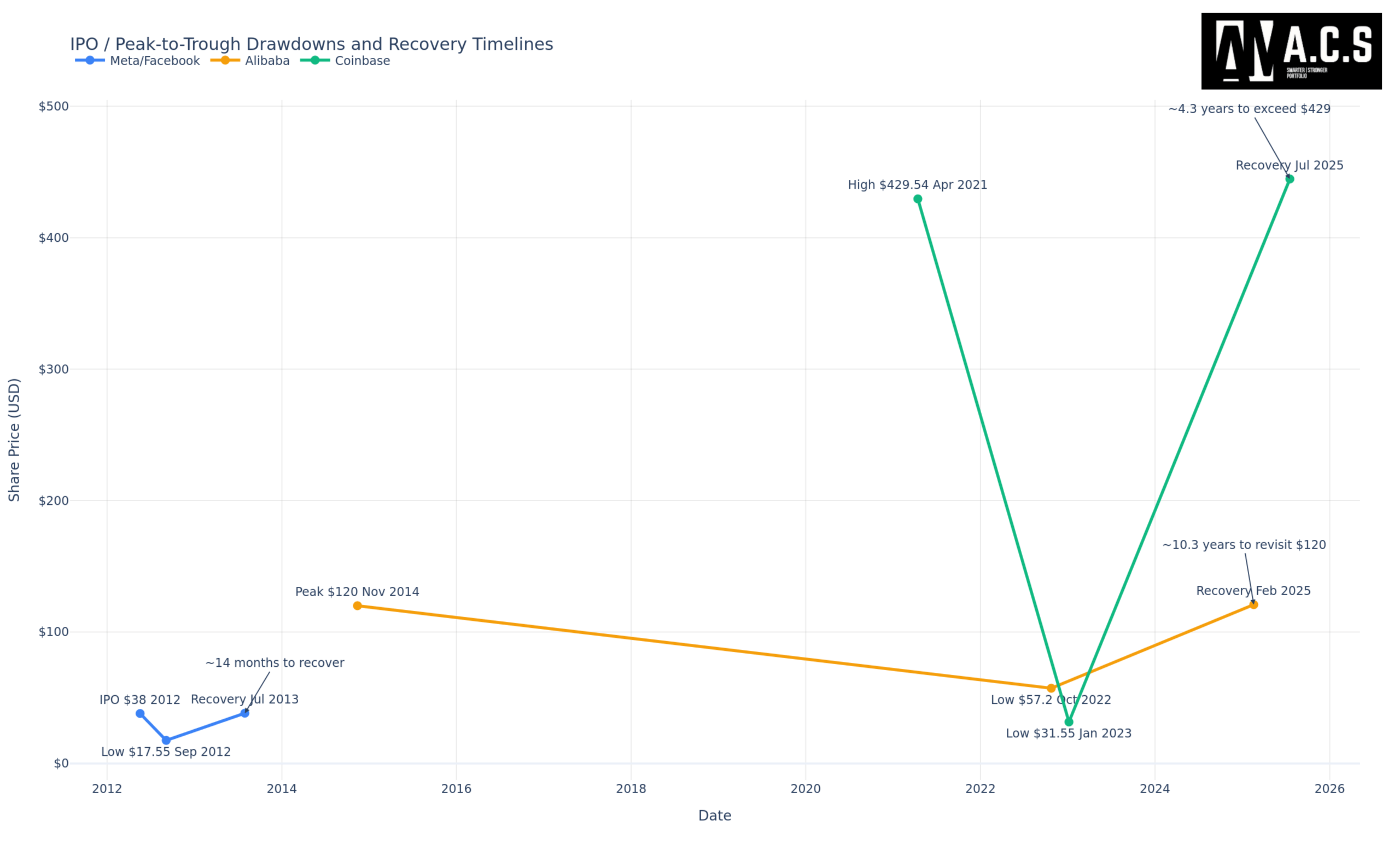

I still remember the feeling. Coinbase went public via direct listing in April 2021 — the future of finance, they said. I watched shares open at $381 on Nasdaq, hit an intraday high of $429.54, and thought, “this is just the beginning.” I felt smart. I refreshed my brokerage app obsessively, watching the numbers climb.

Then it happened. Over the following months and years, COIN collapsed. By late 2022, it touched $32.53 — an intraday low near $31 at its worst. Nearly a 93% drawdown from peak. It took almost four years for the stock to revisit anything close to its debut-day levels.

I wasn’t wrong about Coinbase. It remains the leading US crypto exchange. My thesis was correct. But my timing destroyed my returns. The gap between being right about a company and being right about an entry price is wider than most investors ever admit.

That gap is precisely what concerns me about the SpaceX IPO.

The SpaceX IPO is expected to hit Nasdaq around June 12 under ticker SPCX, targeting a $1.75 trillion valuation with roughly $75 billion in capital raised. It is being called the largest IPO in history — more than double Saudi Aramco’s $29.4 billion record. The headlines are deafening. SpaceX also approved a 5-for-1 stock split in mid-May, dropping the per-share price from roughly $526 to about $105. The message is clear: these shares are being packaged to be affordable. To be bought. To feel like a seat at history’s table.

But here’s what I’ve learned after watching enough of these moments: the louder the narrative, the more important it is to have your own measuring stick. And the lower the per-share price, the easier it is to forget what you’re actually paying for the whole company.

Table of Contents

What’s Actually Inside the SpaceX IPO

If you read only the headlines, you’d think SpaceX is a rocket company going public. The S-1 filing, made public on May 20, 2026, reveals something more complicated — and more important to understand before you commit a single dollar.

The prospectus describes three businesses rolled into one entity. The first is the launch business — Falcon 9, Falcon Heavy, and the emerging Starship program. This is the original SpaceX. Real revenue from government and commercial satellite contracts. A quasi-monopoly on Western orbital launches. But the S-1 reveals it operated at a $619 million loss in Q1 2026 alone. Even the rocket business, the one you think you know, is not printing money.

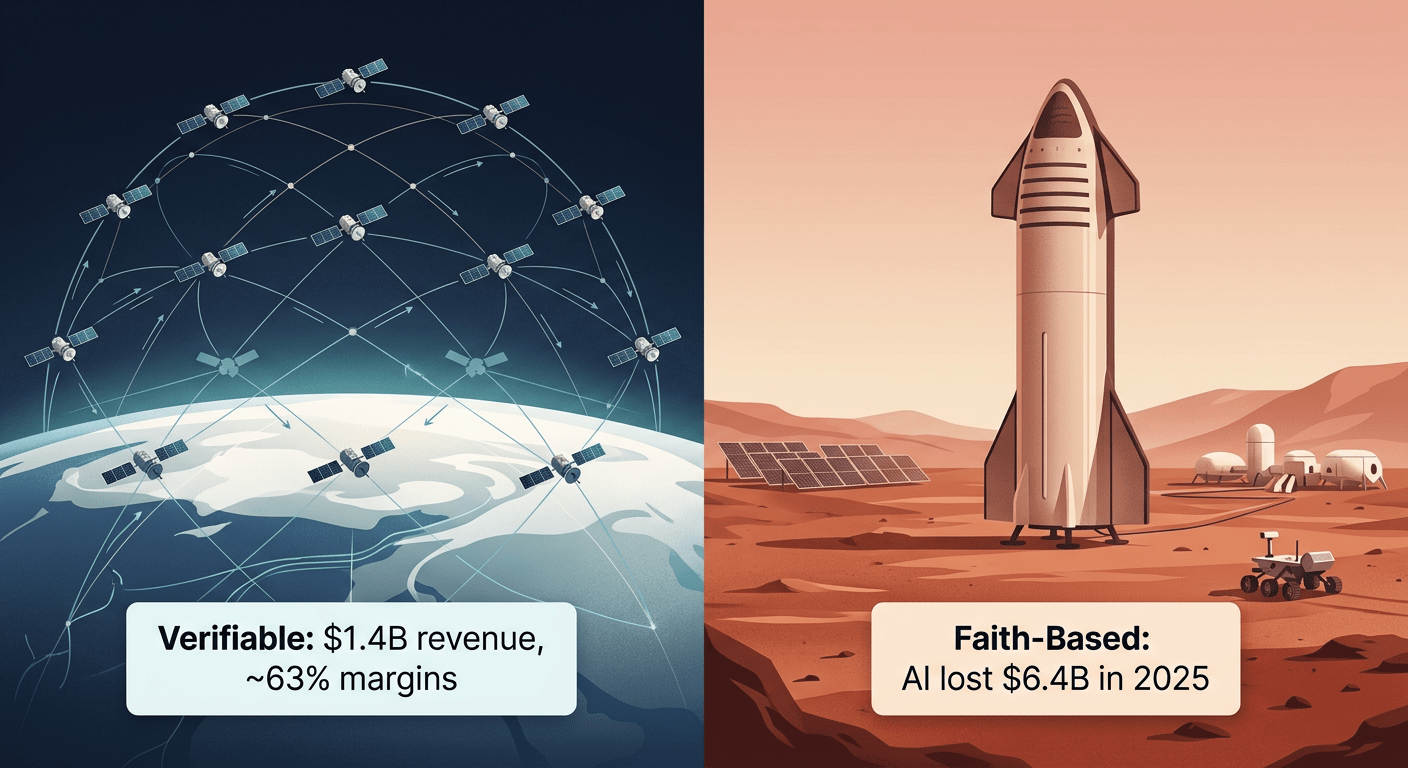

The second is Starlink. In 2025, Starlink generated roughly $11.4 billion in revenue with operating profit around $4.4 billion — the only segment of SpaceX that is genuinely and consistently profitable. Over 10 million users across about 160 countries. But here’s what the S-1 does not clearly advertise: ARPU (average revenue per user per month) has already dropped from $81 to $66. User growth is increasingly concentrated in lower-income regions — Southeast Asia, parts of Latin America — which means per-user spending may continue to decline. User doubling may not translate into revenue doubling. This matters because Starlink is the profit engine. If its per-user economics are softening, the entire “verifiable” half of the thesis weakens.

The third is the part that makes me nervous. In February 2026, Musk merged xAI into SpaceX, creating “SpaceX AI.” This segment burned roughly $6.4 billion in 2025. In Q1 2026 alone, it lost another $2.5 billion on just $818 million in revenue. It consumed $7.7 billion in capital expenditures — in a single quarter. The AI division is also where the Starship program and the long-term Mars colonization vision sit, concepts that, even if directionally correct, have no knowable timeline and no modelable economics.

Consolidated, SpaceX posted total revenue of about $18.7 billion in 2025 — up over 30% year-over-year. But the company swung from a small $791 million profit in 2024 to a net loss close to $4.94 billion. In Q1 2026, it generated over $4.69 billion in revenue and lost $4.28 billion. Its accumulated deficit by March 31, 2026: $41.3 billion.

These are the numbers. What you do with them is your call, but you should at least know they exist before you hear the word “Mars” and reach for your brokerage app.

Why This Matters More Than Any Other IPO

This is not just another hot tech listing. The scale, the mechanics, and the structural oddities are unprecedented — and they directly affect what price you’ll pay and what you’re actually buying.

The valuation is aggressive by any historical yardstick. At $1.75 trillion, SpaceX trades at roughly 93x its trailing 2025 revenue of $18.7 billion. For context: Meta went public at about 28x sales. Google at roughly 10x. Nvidia, the most valuable company on earth right now, trades around 20x forward revenue — and it is massively profitable. We are being asked to pay nearly 5x Nvidia’s multiple for a company that just posted a multi-billion-dollar annual loss. “Big Short” investor Michael Burry put it bluntly after reading the S-1: “Nothing in that filing suggests it is worth $1 trillion, let alone $2 trillion.”

The Nasdaq changed its rules for this. Effective May 1, 2026, Nasdaq modified its Nasdaq-100 index inclusion methodology. The old rule required a three-month waiting period before a new listing could enter the index. The new rule: 15 trading days. The old rule required at least 10% of shares as public free float. The new rule: that minimum is gone entirely. SpaceX, with an estimated 4.3% free float, would have been disqualified under the old framework. The NYSE’s president publicly called the changes “tailor-made,” adding that “market integrity is not a competitive dimension.” FT columnist Robin Wigglesworth described the setup as “the biggest bagholder exercise of all time.” When the exchange itself rewrites its rulebook to accommodate one listing, you should ask whose interests those changes serve.

This directly impacts your entry price. Passive index funds that track the Nasdaq-100 and S&P 500 are mandated to buy any stock added to their benchmark — regardless of valuation. Bloomberg Intelligence estimates roughly $20 to $27 billion in automatic passive demand for SpaceX upon index inclusion. When only about 4.3% of shares are actually trading in the open market — less than $90 billion of stock in a $1.75 trillion company — that concentrated mechanical buying can push prices far beyond what fundamentals justify. This is not a prediction. It’s a mechanical reality.

The Anthropic contract has a credibility problem. The S-1 describes a compute deal worth roughly $1.25 billion per month through May 2029 — about $45 billion total — with AI company Anthropic, using SpaceX’s Colossus data center in Memphis. Within 24 hours of the S-1 filing, during the SEC-mandated quiet period when management is not supposed to materially reinterpret prospectus disclosures, Musk posted on X that the deal was merely a “180-day lease with 90-day notice mutual cancellation thereafter,” capping the implied commitment at roughly $7.5 billion. That is a $37.5 billion gap between the official filing and the CEO’s own characterization. Columbia Law professor Eric Talley summarized the situation: either the S-1 is “materially misleading” or Musk is “up to his old hijinx.” In my experience, when the single largest forward-revenue anchor in the prospectus cannot survive 24 hours of public scrutiny, you need to price that uncertainty into your decision.

Institutional investors are publicly walking away. On May 30, 2026, AkademikerPension — a Danish pension fund managing roughly $25 billion in assets — announced it would blacklist SpaceX entirely, refusing to participate in the IPO at any price. Chief Investment Officer Anders Schelde called the governance structure “catastrophic,” noting that Musk would control approximately 85% of voting power while simultaneously serving as CEO, CTO, and Board Chair. He added they would refuse to invest even if the valuation were reasonable. The fund is not alone: CalPERS, the New York State Common Retirement Fund, and NYC pension funds jointly sent a letter to Musk raising “serious concerns” about what they called an “extreme governance structure.” Musk achieves this control through a dual-class share structure — Class B shares carry 10 votes each while public Class A shares carry 1 vote. You are buying economic exposure with essentially zero governance influence.

The Framework I Use to Evaluate Any Mega-IPO

After watching enough IPOs launch, spike, and crater over the years, I stopped looking for someone else’s verdict and built a simple framework. It is not complicated. It just forces me to be honest about what I am actually paying for.

Split the company into two buckets.

Bucket one: the Verifiable Half. Starlink’s $11.4 billion in revenue at roughly 63% EBITDA margins. The launch monopoly on Western orbital access. The existing government and commercial satellite contracts. These are assets you can model. You can track ARPU trends ($81 → $66 and falling), user growth demographics, margin expansion or contraction. You can form a reasonable, numbers-based opinion about what this half is worth.

Bucket two: the Faith-Based Half. The AI segment burning $2.5 billion per quarter on $818 million in revenue. Starship, which flew only 5 times in 2025 against a 25-flight target and has no stable commercial operation. The Mars colonization vision that could take decades — or never materialize in investable form. The “multi-planetary species” thesis that, however compelling as a human story, has no discountable cash flows. The $28.5 trillion total addressable market claimed in the prospectus — roughly the size of US GDP — that includes asteroid mining, orbital data centers, and lunar energy production.

Now ask yourself: of the $1.75 trillion price tag, how much am I assigning to each bucket? If you think the verifiable half is worth, say, $500 billion, then you are betting $1.25 trillion on faith. That might be a trade you want to make. But at least you would know that is the trade you are making.

Understand the three forces driving post-IPO price.

Force one is emotional hype: day-one euphoria, “largest IPO ever” headlines, Musk’s tweets, the 5-for-1 stock split making shares feel cheap. This force dominates the first days and weeks.

Force two is mechanical flows: passive index fund buying ($20-27 billion estimated), ETF creation, the staggered lock-up expiry calendar. These are price-insensitive — they buy or sell regardless of valuation. Early on, they create artificial upward pressure. Later, when insider lock-ups expire and early investors sitting on massive low-cost-basis gains begin to sell, the mechanical flows reverse.

Force three is fundamental performance: over multiple quarters, the actual numbers — Starlink ARPU trajectory, AI burn rate, Starship milestones, launch contract margins — eventually matter. The pattern I have seen repeatedly is that Force 1 and Force 2 inflate the price early, and Force 3 takes months or years to catch up — or catch down. A great company with strong long-term fundamentals can still produce terrible multi-year returns if you bought during the emotional and mechanical surge.

My secret weapon — the question I ask myself before any IPO — is this: What structural mechanism makes this time different? Not what narrative makes it different. Not “Elon Musk is a genius” or “space is the future.” What mechanical, verifiable market structure prevents the same outcome we saw with Facebook ($38 to $17), Alibaba ($120 to $57), and Coinbase ($429 to $32)?

For SpaceX, I have not found one. The stock split makes shares cheaper, not cheaper on a valuation basis. The Nasdaq rule change makes index inclusion faster, not safer. The 30% retail allocation makes access broader — but as I will explain, that is likely a reflection of need, not generosity.

The Mistakes That Cost Me Years of Returns

Buying the day-one euphoric open.

I have done this. Not once. You watch the price climb in the first hours and feel like a genius. You check your brokerage app during dinner. You calculate what the position would be worth if it “just” doubles. For about four hours, you are a market wizard. Then the afternoon fade begins. Then the overnight gap down. By week three, you are down 25-30%, and you tell yourself you are “long-term” to avoid admitting you timed it terribly. You hold through months of slow bleeding, checking the price every morning with a knot in your stomach, ignoring the position in conversations with friends, until you eventually capitulate near the bottom — often within days of the actual turning point.

The data backs up the pain. According to “The Life Cycle Trade” by Goehring and Rozencwajg, only about 20% of IPOs double in their first year, and over 90% eventually trade below their first-day low at some later point. The IPO price — and especially the day-one open — often becomes a multi-year high, not a starting line. There is no prize for being first. Let a quarter or two of public-market earnings establish a track record before committing meaningful capital.

Confusing the 30% retail allocation with generosity.

The headlines trumpet “unprecedented retail access — up to 30% of IPO shares allocated to individual investors!” What they are less eager to explain: the allocation rose from 20% to 30% because the capital raise target increased from $50 billion to $75 billion. They needed more buyers. Within that 30%, priority goes to private-wealth clients and family offices managing tens of millions or more. Ordinary retail through standard brokerages gets a small subset, and it is heavily oversubscribed — 10 to 20 times expected. If the deal were as attractive as the headlines suggest, institutions would take the entire allocation without hesitation. The retail share exists because it needs to.

Letting the Cerebras warning shot go unexamined.

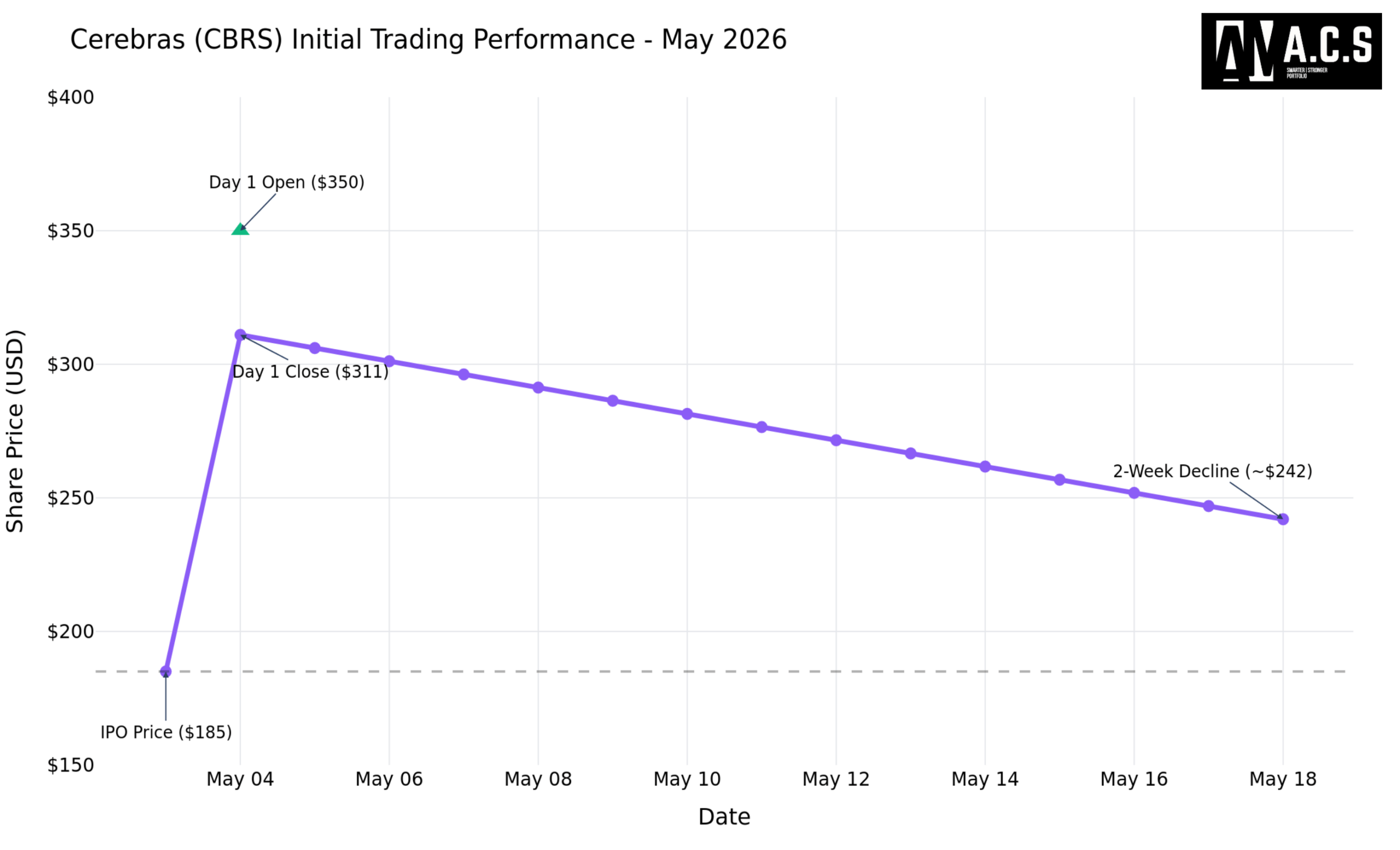

Just weeks before the SpaceX roadshow, AI chip company Cerebras (CBRS) executed the textbook mega-IPO pop-and-drop. Priced at $185 on May 13, 2026. Opened at roughly $350-385 — an 89% pop. Closed day one at $311. Within two weeks, it was trading below $242 — down roughly 22% from the day-one close and about 35% from the euphoric open. The offering was 20x oversubscribed. The fast-tracked S&P index inclusion was announced shortly after. None of it stopped the decline. The pattern is not mysterious. Institutions filled at $185. Retail chased the $350 open. Two weeks later, anyone who bought at the open was nursing a 30% loss on a position they were “sure about.” Anyone who says SpaceX will be different needs to explain what structural mechanism makes it different — not what narrative makes it different, but what mechanical reality prevents the identical outcome.

FAQ: Questions I Keep Getting About This IPO

Should I buy SpaceX on day one?

Historical data strongly suggests waiting. Facebook dropped over 50% from its IPO price before becoming a multi-bagger. Alibaba fell below its issue price and took three years to revisit its early highs. Coinbase collapsed roughly 93% before recovering. Day-one buyers almost always pay the highest price because they are buying at the peak intersection of narrative hype and structural scarcity. The company will still exist in six months. Wait for a few quarters of public-market earnings to establish a track record outside the IPO hype window.

Is SpaceX a good investment at this price?

SpaceX is an extraordinary company. The question is whether it is a great stock at $1.75 trillion. At roughly 93x trailing sales while losing billions per quarter — and with its only profitable segment (Starlink) showing declining per-user revenue — the price already embeds years of flawless execution across every business line, including the ones that do not have stable revenue yet. Even perfect execution may only grow into the valuation, not exceed it. Peter Thiel made his legendary return buying into SpaceX during the 2008 near-bankruptcy, not at the peak of IPO euphoria. The price you pay determines your returns.

How do I actually buy SpaceX stock?

Once listed on Nasdaq under SPCX around June 12, shares will be available through Schwab, Fidelity, Robinhood, SoFi, and E-Trade. The 5-for-1 stock split means the per-share IPO price will be around $105 rather than $526. Just do not confuse accessibility with opportunity. A low nominal share price says nothing about whether the underlying valuation is reasonable.

Final Thoughts

I am not going to tell you to buy SpaceX or not buy it. That is your call, and anyone who gives you a one-sentence verdict on a $1.75 trillion decision framed by the largest financial event in market history is not being honest with you — or with themselves.

What I will tell you is what I am doing. I am not buying on day one. I am not buying in the first week. I am watching the roadshow, tracking the final pricing, and waiting for at least one full quarter of public-market earnings before I form a view on what the verifiable half of this company is actually worth. I need to see Starlink’s ARPU trajectory stabilize. I need to see whether the AI segment’s burn rate has any credible path to breakeven. I need to see whether the Anthropic contract — whatever it actually is — survives a full quarter of scrutiny. And I need to see how the stock trades after the mechanical buying from index inclusion has run its course and the lock-up expiry selling has begun.

In other words: I need a measuring stick. And now you have one too.

The skill of looking at a market event, separating signal from noise, and knowing when to act versus when to wait — that is not something you build from reading one article. It is a muscle. I exercise it daily, across traditional markets and crypto, and I share the frameworks in real-time with people who think the same way.

If you want to keep thinking sharper about markets, I share free IPO breakdowns, macro observations, and investing frameworks in my public channel. And for those ready to apply this same analytical rigor to crypto — where the information asymmetry is bigger and the moves happen faster — I run a private signals channel built on the same principle: framework first, decision second, no hype.

Ready to Take the First Step?

Join our community for daily market news. Curious about our strategy? Preview 8-15 daily short-term trade setups in the Signals channel — new users who join via the "Trade Signals" button automatically receive a $59/month pass. Prefer a personal conversation? Contact us anytime.